As a COO, your primary concern regarding mandatory climate reporting in Singapore is practical: what must actually be done to prepare for mandatory sustainability assurance, and how can the team get ready without disrupting daily operations? This practical operational guide cuts out academic theory to focus purely on the intersection of compliance requirements and execution, providing clear timelines and actionable steps.

The Mandate Explained

It is crucial to understand the critical distinction between ESG reporting and sustainability assurance. ESG reporting simply involves publishing your sustainability data, whereas sustainability assurance is the external audit verifying that your data is accurate. Singapore now requires both processes.

Who Must Comply & When:

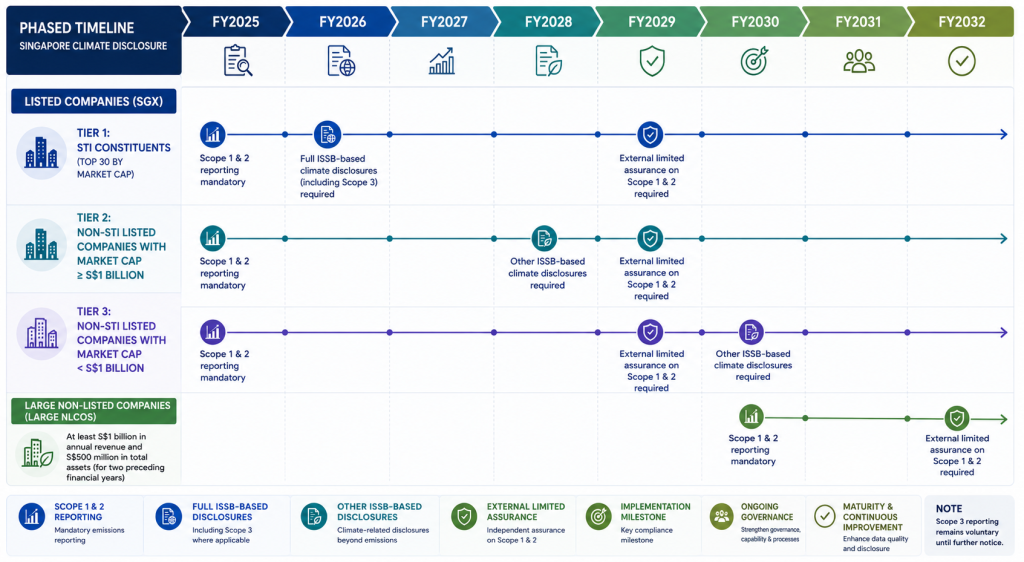

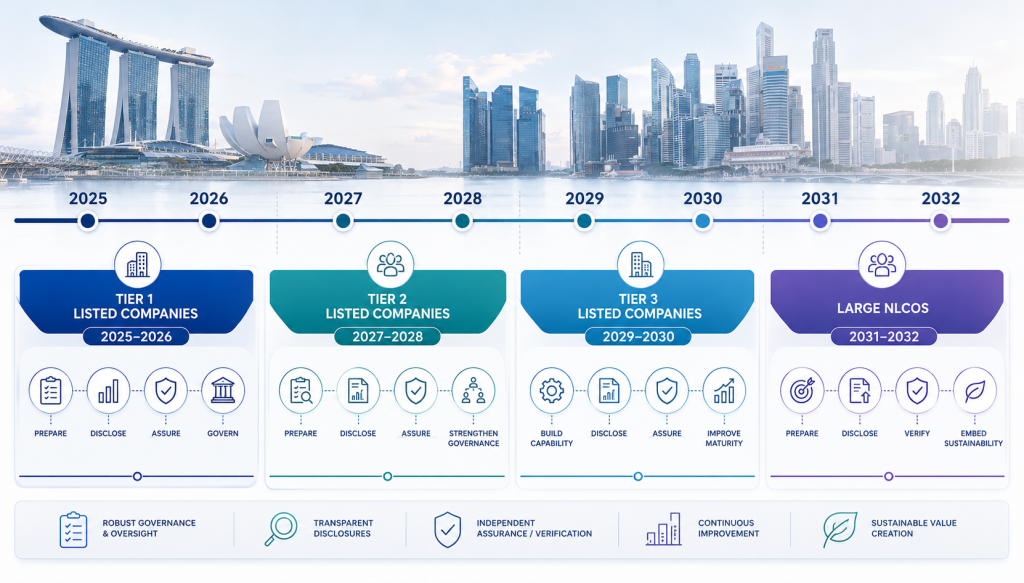

Listed Companies (SGX): Singapore’s framework tiers listed companies into three groups based on market capitalisation:

- STI Constituents (top 30 by market cap): Scope 1 and Scope 2 emissions reporting mandatory from FY2025. Full ISSB-based climate-related disclosures (including Scope 3) required from FY2026. External limited assurance on Scope 1 and 2 required from FY2029.

- Non-STI listed companies with market cap ≥ $1 billion: Scope 1 and 2 reporting from FY2025; other ISSB-based climate disclosures from FY2028; external assurance from FY2029.

- Non-STI listed companies with market cap < $1 billion: Scope 1 and 2 reporting from FY2025; other ISSB-based climate disclosures from FY2030; external assurance from FY2029.

Large Non-Listed Companies (Large NLCos): Organisations with at least $1 billion in annual revenue and $500 million in total assets (for two preceding financial years) must begin Scope 1 and 2 reporting from FY2030, with external limited assurance required from FY2032. Scope 3 reporting remains voluntary until further notice.

ASEAN Subsidiaries: Your regional branches may need separate compliance workflows depending on their parent-subsidiary reporting structure. Subsidiaries whose parent already files ISSB-based or equivalent reports (e.g., European Sustainability Reporting Standards) and whose activities are included in those consolidated reports may qualify for a permanent exemption.

Why This Matters Now

The ISSA 5000 standard, published by the IAASB in November 2024, becomes effective for sustainability assurance engagements for periods beginning on or after December 15, 2026 (early adoption is permitted). Building systems that are ready for assurance takes 12 to 18 months, meaning a delayed start leads to a rushed implementation and much higher costs.

A significant readiness gap exists across the market. Singapore’s carbon tax also adds commercial urgency: the carbon price rises from $25 per tonne in 2025 to $45 per tonne in 2026–2027, targeting $50–$80 per tonne by 2030. Accurate GHG accounting is no longer purely a compliance exercise, it directly affects tax liabilities.

What Actually Changes in Your Operations

Achieving assurance readiness means transitioning from “good enough reporting” to building completely audit-proof systems.

1. Data Collection Transformation You must transition from using simple estimates and spreadsheets to capturing verified measurements with strict audit trails. For example, you cannot just state that you emitted “1,000 tons of CO2”; you must explicitly prove it using meter readings, supplier invoices, and traceable calculations.

2. Internal Controls Requirements You will need to heavily document who collects the data, who verifies it, and who approves it. Auditors will demand strict segregation of duties, meaning the same person cannot both collect and approve the data. You must also establish regular reconciliation and validation processes.

3. Technology & Process Upgrades Your operations will require new GHG emissions tracking systems and robust document management solutions for holding audit evidence. These tools must integrate seamlessly with your existing fleet management, energy systems, and procurement workflows.

4. Skills & Capability Gaps Your team will need to build sustainability accounting expertise, deep internal controls knowledge, and strong data management competency. The ultimate challenge for a COO is implementing these changes while maintaining operational excellence.

“Most COOs treat this as a finance/compliance project. It’s actually an operations transformation project that needs your direct leadership.”

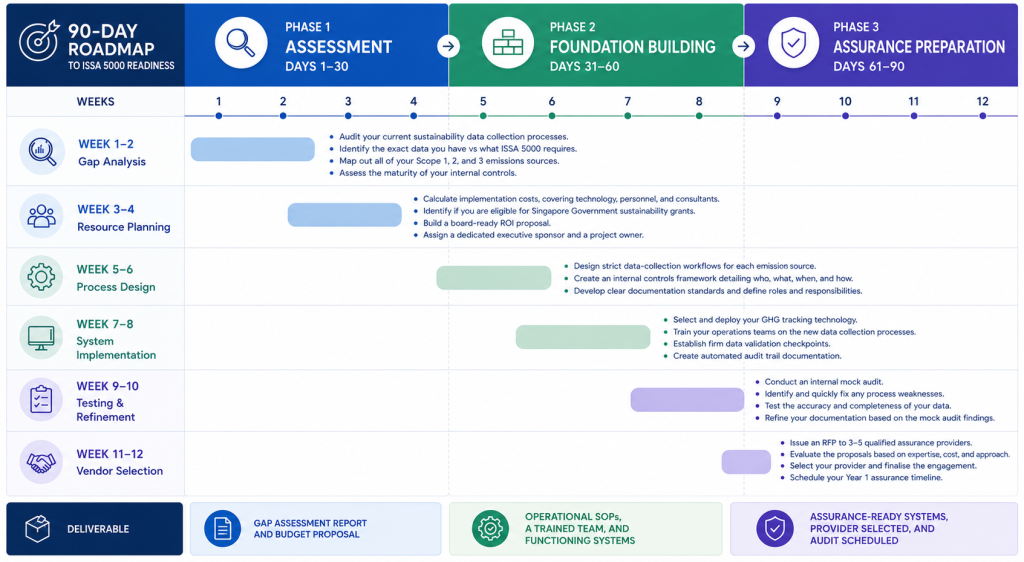

The 90-Day Readiness Roadmap

Phase 1: Assessment (Days 1–30)

Week 1–2: Gap Analysis

- Audit your current sustainability data collection processes.

- Identify the exact data you have versus what ISSA 5000 requires.

- Map out all of your Scope 1, 2, and 3 emissions sources.

- Assess the maturity of your internal controls.

Week 3–4: Resource Planning

- Calculate implementation costs, covering technology, personnel, and consultants.

- Identify if you are eligible for Singapore Government sustainability grants (see Grant Funding Strategy below).

- Build a board-ready ROI proposal.

- Assign a dedicated executive sponsor and a project owner.

Deliverable: Gap assessment report and budget proposal.

Phase 2: Foundation Building (Days 31–60)

Week 5–6: Process Design

- Design strict data-collection workflows for each emissions source.

- Create an internal controls framework detailing who, what, when, and how.

- Develop clear documentation standards and define roles and responsibilities.

Week 7–8: System Implementation

- Select and deploy your GHG tracking technology.

- Train your operations teams on the new data collection processes.

- Establish firm data validation checkpoints.

- Create automated audit trail documentation.

Deliverable: Operational SOPs, a trained team, and functioning systems.

Phase 3: Assurance Preparation (Days 61–90)

Week 9–10: Testing & Refinement

- Conduct an internal mock audit.

- Identify and quickly fix any process weaknesses.

- Test the accuracy and completeness of your data.

- Refine your documentation based on the mock audit findings.

Week 11–12: Vendor Selection

- Issue an RFP to 3–5 qualified assurance providers.

- Evaluate the proposals based on expertise, cost, and approach.

- Select your provider and finalise the engagement.

- Schedule your Year 1 assurance timeline.

Deliverable: Assurance-ready systems, provider selected, and audit scheduled.

Estimated Resource Requirements Summary

| Company Size | Estimated Budget | Team FTEs | Timeline |

| $10–30M | $50–80K | 0.5–1 FTE | 90–120 days |

| $30–100M | $80–150K | 1–2 FTEs | 120–180 days |

| $100M+ | $150–300K | 2–3 FTEs | 180–240 days |

Building the Business Case for Your Board

When seeking board approval, use an ROI framework that highlights avoided costs and newly created value.

Compliance Benefits (Avoid Costs): Proactive compliance helps you avoid regulatory penalties and mitigates reputational risk. It also ensures you are completely ready for investor ESG due diligence.

Operational Benefits (Create Value): Better data tracking leads to energy-efficiency insights that reduce costs. It also helps identify supply chain optimisation opportunities and hidden process improvements.

Strategic Benefits (Long-term Value): Robust ESG practices enhance your enterprise valuation for M&A and fundraising, typically yielding a 10–20% ESG premium. It builds stronger stakeholder trust, brand equity, and provides a competitive advantage in sustainability-focused tenders.

Grant Funding Strategy

To structure your project for maximum funding:

- Sustainability Reporting Grant (SRG): Launched by EDB and EnterpriseSG, the SRG co-funds up to 30% of qualifying costs, capped at $150,000, for a company’s first ISSB-aligned sustainability report. Available to all SGX-listed companies (regardless of size) and non-listed companies with annual revenue of at least $100 million. Apply via the Business Grants Portal.

- Enterprise Development Grant (EDG): Supports larger sustainability transformation projects, carbon reduction programmes, green certifications, and sustainable process redesign. Standard support is up to 50% for SMEs and 30% for non-SMEs. Apply before 31 March 2026 if you want the enhanced 70% sustainability rate (where still eligible).

- CTC Grant: Utilise to build internal ESG and capability competencies within your team, available until 31 July 2026 (subject to fund availability).

- SME Sustainability Reporting Programme: For SMEs with revenue below $100 million that want to prepare early, EnterpriseSG partners with service providers to offer advisory at cost-competitive rates 70% defrayed for applications from November 2024 to March 2026, and 50% from April 2026 to October 2027.

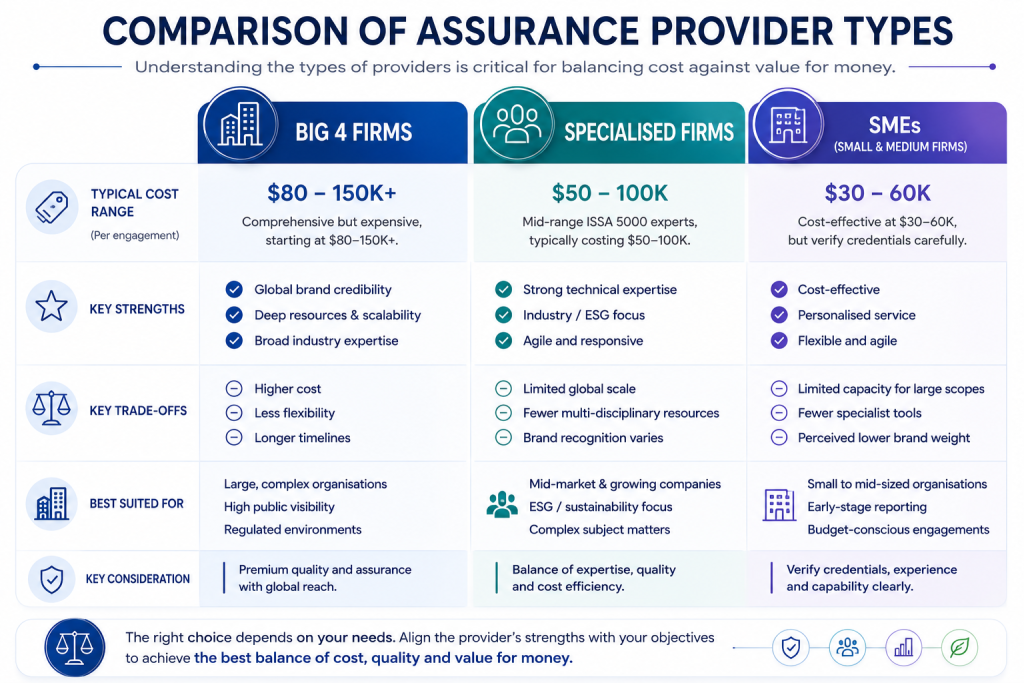

Selecting Your Assurance Provider

Understanding the types of providers is critical for balancing cost against value for money.

- Big 4 Firms: Comprehensive but expensive, starting at $80–150K+.

- Specialised Firms: Mid-range ISSA 5000 experts, typically costing $50–100K.

- SMEs/Regional Firms: Cost-effective at $30–60K, but verify credentials carefully.

Note that, external assurance must be provided by a registered climate auditor, either an ACRA-registered audit firm or a testing, inspection and certification (TIC) firm accredited by the Singapore Accreditation Council (SAC).

Key Selection Criteria: Ensure the provider has completed training and a track record in ISSA 5000 expertise. They must understand your industry’s operations and be compatible with your current systems. If you have regional operations, ASEAN knowledge is highly important.

The 5 Questions to Ask Every Provider:

- How many ISSA 5000 engagements have you completed?

- What is your approach to assessing our internal controls?

- How will you coordinate with our operations teams?

- What technology platforms do you work with?

- Can you provide a fixed-price versus a time-and-materials proposal?

Red Flag: Be cautious of providers who promise a “quick and easy” audit; assurance is rigorous by design.

Your 30-Day Action Plan

Week 1: Education

- Share this guide with your CEO, CFO, and Board.

- Schedule a 2-hour alignment workshop.

- Assign an executive sponsor.

Week 2: Assessment

- Conduct a rapid gap assessment.

- Identify your top 3 critical gaps.

- Generate a rough cost estimate.

Week 3: Planning

- Develop a project charter.

- Create a budget proposal with your calculated ROI.

- Research your eligibility for the SRG, EDG, and CTC grants.

Week 4: Approval & Launch

- Present your proposal to the board for approval.

- Initiate the vendor selection process.

- Kick off Day 1 of your 90-day roadmap.

Ready to start? Download our 30-Day Assurance Readiness Kickstart Checklist. Not sure where to start? Book a free 30-minute assessment with Mayuresh.

Frequently Asked Questions

Q1: Is sustainability assurance already mandatory for Singapore listed companies?

Not yet for assurance, but reporting is. All SGX-listed companies have been required to report Scope 1 and Scope 2 GHG emissions from FY2025. External limited assurance on those emissions becomes mandatory for all listed companies from FY2029. Use the time between now and then to build the internal controls and data quality that assurance providers will require.

Q2: Does my large non-listed company need to comply with the same timeline as listed companies?

No. Following ACRA and SGX RegCo’s August 2025 update, large non-listed companies (annual revenue ≥ $1 billion and total assets ≥ $500 million) must begin Scope 1 and 2 climate reporting from FY2030, with external assurance required from FY2032. This gives you more lead time than listed companies, but starting your readiness work now still pays dividends in cost savings and smoother implementation.

Q3: What is ISSA 5000 and why does it matter to my company?

ISSA 5000 is the new global standard for sustainability assurance, issued by the International Auditing and Assurance Standards Board (IAASB) in November 2024. It becomes effective for periods beginning on or after 15 December 2026. Your assurance provider will be required to conduct their engagement under this standard, which means your internal data systems, controls, and documentation must be designed to withstand ISSA 5000-level scrutiny. Singapore is expected to formally adopt the standard.

Q4: What’s the difference between limited and reasonable assurance?

Limited assurance (negative assurance) means the auditor found no material issues after a moderate level of testing, it’s the level Singapore currently mandates. Reasonable assurance (positive assurance) is equivalent to a full financial audit and requires more extensive testing. Most companies will start with limited assurance, which is still rigorous and requires strong underlying data systems.

Q5: What grants are available to help cover our sustainability assurance costs?

The most directly relevant grant for compliance preparation is the Sustainability Reporting Grant (SRG), which covers up to 30% of qualifying costs (capped at $150,000) for your first ISSB-aligned report. For broader sustainability transformation projects, the Enterprise Development Grant (EDG) provides up to 50% support for SMEs. The CTC Grant can fund internal capability building. Check current eligibility criteria on the Business Grants Portal, as grant terms and deadlines are updated regularly.

Q6: Can a non-accounting firm conduct our sustainability assurance?

Yes, under Singapore’s framework, external assurance can be performed by either an ACRA-registered audit firm or a testing, inspection and certification (TIC) firm accredited by the Singapore Accreditation Council. However, always verify that your chosen provider has demonstrable ISSA 5000 competency and, where relevant, sector-specific expertise.

Q7: Our ASEAN subsidiary is covered by our parent company’s sustainability report. Do we still need to comply?

Possibly not. ACRA has introduced a permanent exemption for non-listed companies whose parent (local or foreign) already prepares climate or sustainability reports using ISSB-based or equivalent standards (e.g., ESRS) and whose activities are included in those consolidated reports, which must be publicly available. Verify your eligibility directly against ACRA’s current exemption criteria before assuming you are covered.

Q8: What happens if we miss the mandatory reporting or assurance deadline?

Singapore’s framework includes penalties for non-compliance. Beyond regulatory fines, late or absent disclosure creates significant reputational risk with investors, lenders, and tender evaluators, all of whom increasingly use ESG disclosures in their due diligence. The reputational and financial cost of non-compliance typically far exceeds the cost of early preparation.

References

- Accounting and Corporate Regulatory Authority (ACRA) and Singapore Exchange Regulation (SGX RegCo). (25 August 2025). Extended Timelines for Most Climate Reporting Requirements to Support Companies. https://www.acra.gov.sg/news-events/news-announcements/887/

- Accounting and Corporate Regulatory Authority (ACRA). Sustainability Reporting and Assurance Requirements. https://www.acra.gov.sg/regulations/sustainability-reporting/requirements-timeline/

- Accounting and Corporate Regulatory Authority (ACRA). Climate Reporting and Assurance Roadmap in Singapore (Official PDF). https://www.acra.gov.sg/docs/default-source/default-document-library/sustainability-reporting/climate-reporting-and-assurance-roadmap-in-singapore.pdf

- International Auditing and Assurance Standards Board (IAASB). (November 2024). International Standard on Sustainability Assurance (ISSA) 5000, General Requirements for Sustainability Assurance Engagements. Effective for periods beginning on or after 15 December 2026. https://www.iaasb.org/publications/international-standard-sustainability-assurance-5000-general-requirements-sustainability-assurance

- IAASB. ISSA 5000 Adoption and Implementation. https://www.iaasb.org/consultations-projects/issa-5000-adoption-and-implementation

- Allen & Gledhill. (September 2025). ESG Quick Guide: Singapore — Mandatory Climate Reporting Regime. https://sustainablefutures.linklaters.com/post/102l789/esg-quick-guide-singapore-mandatory-climate-reporting-regime

- Allen & Gledhill. (2025). ACRA and SGX RegCo Extend Timelines for Most Climate Reporting Requirements. https://www.allenandgledhill.com/sg/publication/articles/31136/acra-and-sgx-regco-extend-timelines-for-most-climate-reporting-requirements

- EnterpriseSG. Sustainability Reporting Grant (SRG). https://www.enterprisesg.gov.sg/financial-support/sustainability-reporting-grant

- Grantla. (March 2026). Sustainability Grants Singapore 2026: EEG, SRG, EDG, Green Financing. https://grantla.com/guides/sustainability-grants-singapore/

- RSM Singapore. (March 2025). Preparing for ISSA 5000: How to Ensure Readiness for Sustainability Assurance. https://www.rsm.global/singapore/insights/preparing-issa-5000-how-ensure-readiness-sustainability-assurance-evolving-global-landscape

- Benhke SGS. (March 2026). SGX Sustainability Reporting: A New Era of Mandatory Disclosure. https://benhkesgs.com/sgx-sustainability-reporting-a-new-era-of-mandatory-disclosure/

- Anthesis Group. (October 2025). Singapore Sustainability Reporting: Preparing for Mandatory ISSB Climate Disclosures. https://www.anthesisgroup.com/insights/sustainability-reporting-singapore-how-to-prepare-for-mandatory-climate-reporting-to-the-issb-standards/